Skip to content

Skip to content

David, a 67-year-old retired history teacher from Ohio, thought he had his retirement figured out. Like millions of other Americans, he had been on the same Medicare Advantage plan since 2023. It worked, his doctor was in-network, and his monthly premiums were predictable.

“If it isn’t broken, don’t fix it,” David used to say.

But on January 14th, 2026, David walked into his local pharmacy to pick up his routine blood pressure medication. Usually, his copay was $15.

The pharmacist looked at the screen, hesitated, and said, “That will be $142, David.”

David was stunned. “There must be a mistake,” he insisted. But there wasn’t. For the 2026 plan year, his insurance provider had moved his specific medication to a higher “tier,” and his local pharmacy—the one he’d used for twenty years—was no longer a “preferred provider.”

The Great 2026 Overhaul

What David didn’t realize is that 2026 is the year of the most significant Medicare changes in over a decade. With the new $2,100 annual out-of-pocket cap on prescription drugs and the standard Part B premium shifting to $202.90, insurance companies have completely rewritten their playbooks. Plans are dropping doctors, changing pharmacy networks, and shifting drug costs to balance their own budgets.

“I felt like the floor had dropped out from under me,” David shared. “I almost had to cancel our 40th-anniversary trip just to cover my meds for the next three months.”

The Turning Point

Determined not to let his savings drain away, David spent three days researching the new 2026 CMS guidelines. He realized that the “Fine Print” everyone ignores was actually a roadmap to massive savings—if you knew where to look.

He developed a simple 5-Point Verification Checklist to ensure he never faced a “January Surprise” again. By using this list, David discovered a different 2026 plan in his zip code that not only covered his meds for a $10 copay but also included a $150 monthly credit for groceries and dental care.

“I saved over $3,400 for the year just by verifying five simple things,” David says. “Most seniors are leaving this money on the table simply because they don’t know the rules changed on January 1st.”

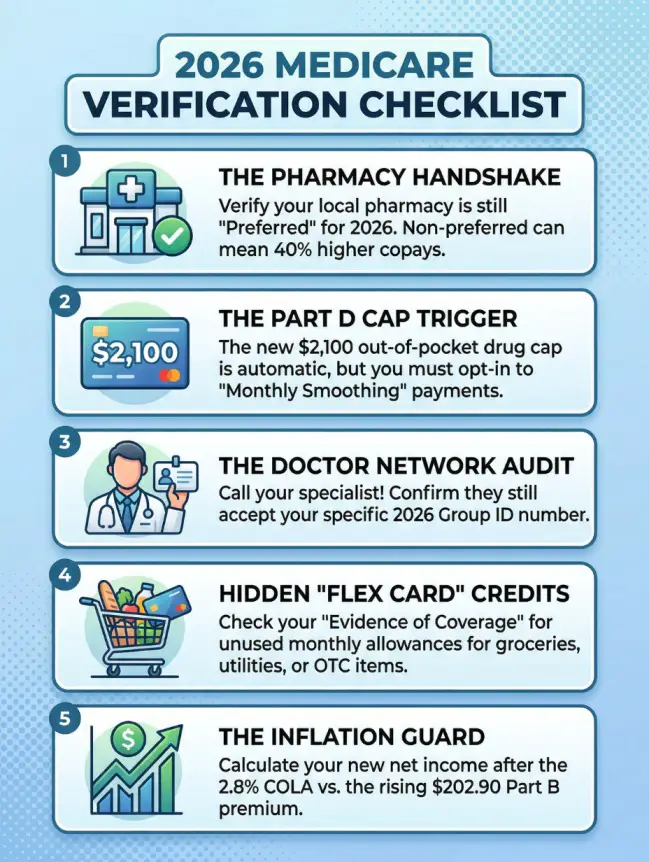

The 5-Point Verification Checklist

This is where the “educational value” happens. For Taboola and Facebook, providing specific, actionable advice is the key to maintaining a high “Quality Score” and keeping your CPC low.

David’s 5-Point “Safety Net” for 2026

If you are over 60, don’t wait for a surprise at the pharmacy counter. Use this checklist to verify your coverage before the next billing cycle.

1. The “Preferred” Pharmacy Handshake In 2026, many major plans shifted their “Preferred” status. If your current pharmacy is now “Standard,” you could be paying 40% more for the exact same pill.

- Action: Call your pharmacist and ask: “Is my 2026 plan still considered ‘Preferred’ at this location?”

2. The $2,100 Out-of-Pocket “Trigger” 2026 introduced a historic cap: you won’t pay more than $2,000 to $2,100 (depending on your specific Part D plan) for covered drugs all year. However, most seniors don’t know about the “Monthly Smoothing” option.

- Action: Ask your provider about the “Medicare Prescription Payment Plan.” It allows you to spread large drug costs into manageable monthly installments instead of one giant bill in January.

3. The “Provider Churn” Audit Because of rising costs, many doctors and specialists opted out of certain Advantage networks for 2026. David found that his cardiologist was still in-network, but the imaging center he used for tests was not.

- Action: Do not rely on last year’s directory. Call your specialist’s office directly and verify they accept your specific 2026 Group ID number.

4. The “Hidden” Flex Card Credits Many 2026 plans have added or increased “Flex Credits” for groceries, utilities, and over-the-counter (OTC) items like toothpaste and aspirin. Some plans offer up to $150 per month in credits that expire if you don’t use them.

- Action: Check your “Evidence of Coverage” for OTC Allowances. Many seniors are literally throwing away $1,000+ a year in free household supplies.

5. The Inflation Guard (COLA vs. Part B) With the 2026 Social Security cost-of-living adjustment (COLA) at roughly 2.8%, and the Part B premium sitting at $202.90, your net “take-home” check may have changed.

- Action: Calculate your new net income. If the Part B increase eats too much of your COLA, you may qualify for a Medicare Savings Program (MSP) that pays your premiums for you.

Final Conclusion

“I used to think Medicare was a ‘set it and forget it’ program,” David says, reflecting on his $3,400 savings. “But the truth is, the rules change every single year. Taking thirty minutes to run through this checklist was the best ‘hourly wage’ I ever earned in my life.”

Don’t leave your retirement to chance. Whether you use a professional comparison tool or call your current provider, make sure you verify these five points today.

Resource Corner

If you want to stay organized like David, here are a few highly-rated tools we recommend:

- The “2026 Senior Medical Planner”: A brilliant downloadable PDF to keep all your 2026 doctor notes and plan changes in one binder.

- “Medicare for Dummies (2026 Edition)“: The essential guide to navigating the new $2,100 drug cap and premium shifts.

Frequently Asked Questions (The “Senior Deep Dive”)

Many readers have reached out with specific questions about David’s checklist. Here are the top three things you need to know about the 2026 changes:

Q1: Is the $2,100 drug cap automatic, or do I need to apply?

A: The cap itself is automatic for all Part D plans in 2026. Once your out-of-pocket spending hits the limit, your plan pays 100% of your covered drug costs for the rest of the year. However, if you want to use the “Monthly Smoothing” option to avoid a large bill in January, you must contact your provider to opt-in to the Medicare Prescription Payment Plan.

Q2: What happens if my doctor leaves my Advantage network mid-year?

A: This is a common fear. If your doctor leaves the network, you generally cannot change plans until the next Open Enrollment period unless you qualify for a Special Enrollment Period (SEP). This is why David’s Point #3 (the Provider Audit) is so critical to do before the enrollment deadlines pass.

Q3: Can I really get “Free” groceries through my 2026 plan?

A: It depends on your plan and your health status. Many “Special Needs Plans” (SNPs) and high-rated Advantage plans in 2026 offer healthy food allowances as part of their “Supplemental Benefits.” These are often loaded onto a “Flex Card.” If you haven’t checked your mail for a new 2026 card, you might be sitting on hundreds of dollars in unused credits.